The Dec. 31, 2025, expiration of many provisions of the 2017 Tax Cuts and Jobs Act (TCJA) adds a new task to the 2025 congressional to-do list: updating the tax code. Many TCJA provisions provided important relief for farm families. While reductions in the corporate income tax rates were made permanent in 2017, income tax cuts for individuals began to phase out in 2022, with the biggest tax increases coming with expirations at the end of 2025.

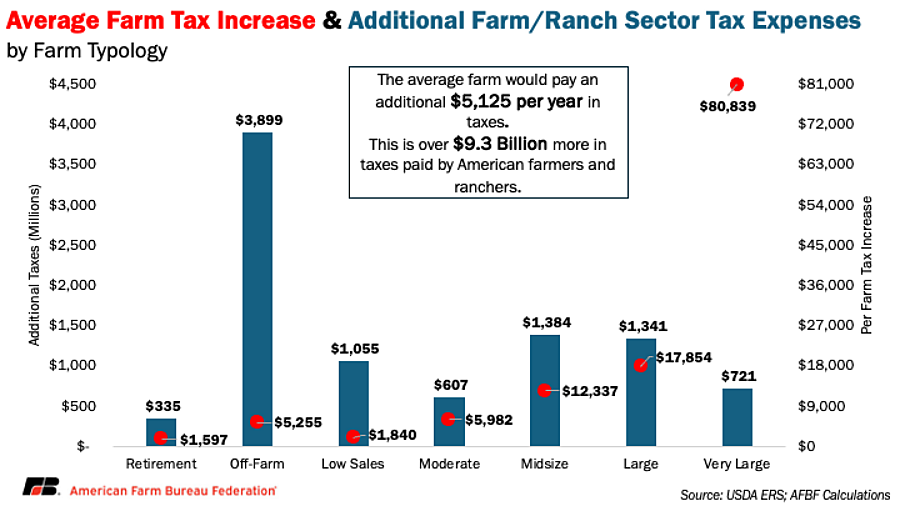

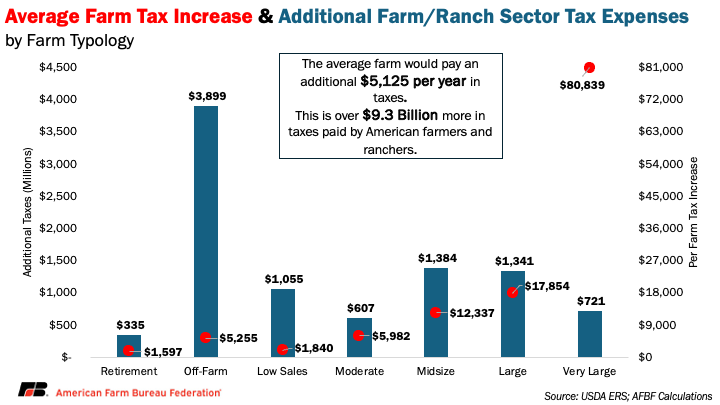

At a time when so many farmers and ranchers are facing razor-thin margins at best and considerable losses at worst, congressional action – or inaction – on tax policy will be a make or break in farm country. Farm families of all sizes were among the 65% of Americans with lower federal taxes after TCJA was passed. If TCJA expires, USDA estimates that farmers and ranchers will spend an additional $9 billion on federal taxes each year.

The size of a federal tax bill can make or break farm profitability, particularly for small farms on the brink of breaking even. Each dollar that comes out of a farm family’s bank account to pay taxes is one less they can spend on improvements to their homes and farms, one less to hire an additional worker, one less to spend at other businesses in their community and one less they can put toward growing food, fiber and fuel.

Property taxes and fees reached record levels in 2024, and federal income taxes are set to soar in 2026 – rising by more than $5,000 per farm on average – due to the temporary nature of the TCJA provisions. This huge tax increase comes on top of above-average production expenses and low crop prices.

Moderate farms are the first group of farmers to make a profit, and that profit is, on average, less than $45,000, even in favorable economic conditions. That means over 13% of their already meager profits would be eaten up by higher taxes. These farms especially are having to make significant capital investments in their operations without the revenues to cover them.

Tax hikes could lead to less production and potential job cuts because assets would have to be diverted from the farm or ranch to pay a federal tax. EY estimates that expiration of TCJA provisions would lead to agriculture losing 49,000 jobs equaling $3 billion in wages and reduce overall economic activity by $10 billion.

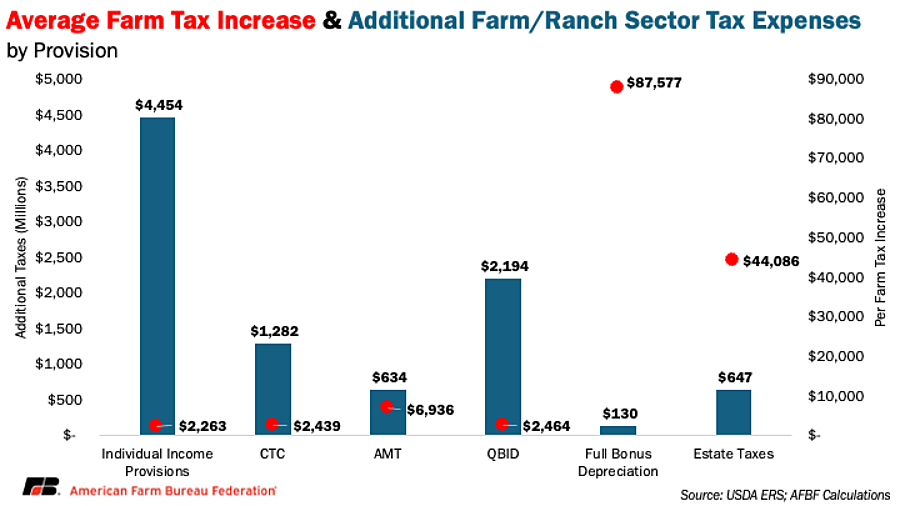

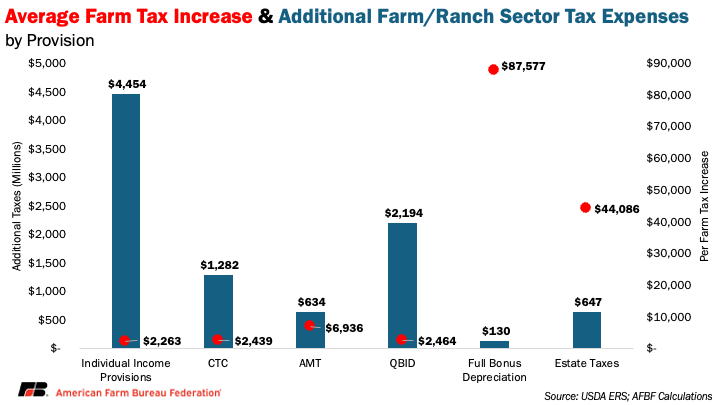

Other than Section 179 capital expensing, all other tax provisions crucial to farm and ranch families are set to revert to permanent law at the end of the year. Larger family farms are generally affected by even more of the expiring provisions like bonus depreciation and estate taxes since they require more capital assets to operate. These bigger family farms, however, are still facing the losses and thin margins that come with high production costs and low revenues, while also contributing more agricultural products for the supply chain than their small counterparts.

The effects of increased taxes described above are only for farms and ranches, but expiration of TCJA tax provisions would likely have ripple effects through the entire ag supply chain and rural communities. These are not only many of the jobs that help sustain farms and ranches in down ag economies, but the feed stores, grain elevators and equipment mechanics needed for the whole agricultural supply chain.

Tax Provisions Benefiting Farmers, Ranchers and Rural Businesses (Title XI, “The One Big Beautiful Bill”):

Permanency of 2017 Individual Tax Code Provisions: Nearly 98% of farms and ranches operate as sole proprietorships, partnerships or S-corporations and did not benefit from the permanent tax relief granted to corporations in 2017. H.R. 1 grants permanency to numerous tax provisions important to families and farms in Title XI, Part 1, preventing their tax rates from increasing if left to expire at the end of 2025. These provisions include expanded tax brackets with a lower maximum tax rate, a doubled standard deduction and child tax credit and increased thresholds for Alternative Minimum Tax (AMT) liability. The bill goes a step further to temporarily enhance some provisions, adding $1,000 per individual to the standard deduction and $500 per child to the child tax credit through 2028.

Qualified Business Income Deduction (Section 199A): For pass-through entities, H.R.1 makes permanent – and improves – the 20% qualified business income deduction introduced in 2017. Starting in 2026, the deduction would increase to 23% of business income with adjustments to allow the deduction to phase-out more slowly for high earners. This lowers the share of farming profits spent on taxes and is a big win for small businesses nationwide that compete alongside corporations with lower tax rates.

Estate Tax Relief for Family Farms: H.R.1 makes the estate tax exemption permanent at $15 million per individual (or $30 million per couple), indexed for inflation. Without this change, the exemption was set to drop back to $5.5 million after 2025, a level that’s wildly out of step with today’s farm economy. With skyrocketing land values, equipment costs and input prices, even modest-sized farms can easily exceed that threshold, meaning upon the owner’s death, far more family operations would face massive tax bills than previously estimated. By locking in a higher, inflation-adjusted exemption, the bill helps ensure more family farms can transition smoothly to the next generation without being forced to sell off land or assets to pay the IRS.

Enhanced Business Expensing and Depreciation:The bill raises Section 179 small business expensing limits to $2.5 million (up from about $1.29 million), with a higher phase-out threshold of $4 million. In addition, H.R. 1 restores full bonus depreciation for capital investments in 2025 through 2029, canceling the remaining phase-down of this expensing benefit. Practically, these provisions mean farmers can continue to write off the entire cost of new equipment, land improvements like drainage tile, modernized barns and other essential capital upgrades in the year of purchase, rather than depreciating them over many years.

In addition, H.R.1 delivers practical tax relief that matters on the ground. Higher thresholds for 1099-K reporting reduce unnecessary paperwork for farms that hire independent contractors or custom services. And by extending key biofuel and renewable energy credits, the bill lowers the cost of on-farm energy projects from biodiesel blending to manure-to-methane systems. Together, these updates cut red tape, reduce expenses and support farmers as they manage razor-thin margins.

Conclusion

Most farming risks, like markets and weather, are out of farmers’, ranchers’ and Congress’ hands, but there is something that can be done about current policy-driven risks like the TCJA expirations and an outdated farm bill. Farm families already face several unknowns on their balance sheet from labor costs and yearly revenues; policy permanency, particularly with a favorable tax code, is one way policymakers can provide a bit of stability for the 2% of Americans providing food, fiber and fuel for our nation and the world.

###

AFBF – Market Intel

{kind=link}

{kind=link}